Economic Self-Destruction Has Re-Entered the Chat

May 26, 2025

Subscribe to our newsletter (for free)

Get the latest articles delivered right to your inbox.

It was another busy week in Trumpworld, with two large news items that are rattling markets. The spectre of economic delusion looms over the White House again.

The Big Beautiful Bill

Let’s start first with Trump’s big tax plan, which narrowly passed the House this week. Given the quintessentially Trumpian title the “One Big Beautiful Bill Act”, the bill is significant for two reasons.

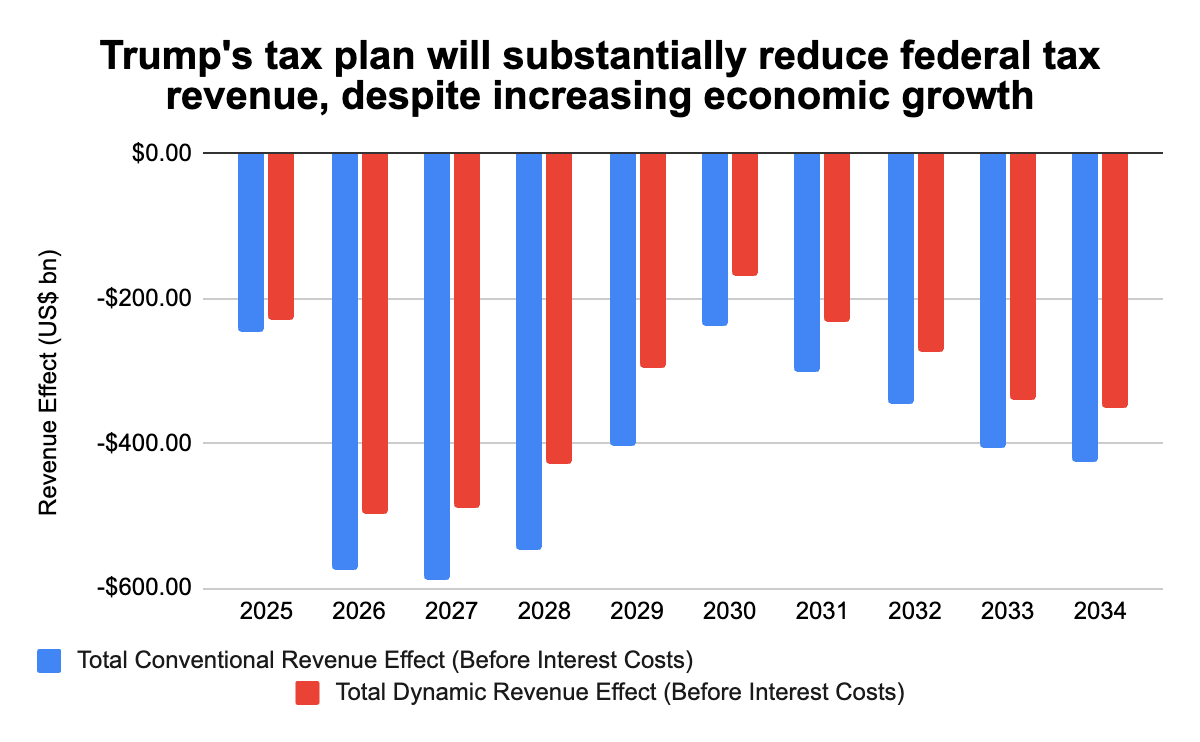

The first is that Republicans seem to have abandoned their ideological commitment to budgetary prudence. The bill, which rolls over Trump’s tax cuts from 2017 on individual income tax and throws in some campaign goodies such as zero tax on tips and overtime work, and higher military and border security spending, is set to substantially increase the size of the US fiscal deficit. An analysis by the Committee for a Responsible Budget forecasts that it will increase the US deficit by $3.1 trillion over the next decade, pushing America’s debt to GDP ratio from 98% to a historic high of 125%. So much for the party of fiscal discipline.

We discussed some of these issues in our livestream show Think Tank Thursdays. Listen here or tune in next time for more similar analysis and quick takes here.

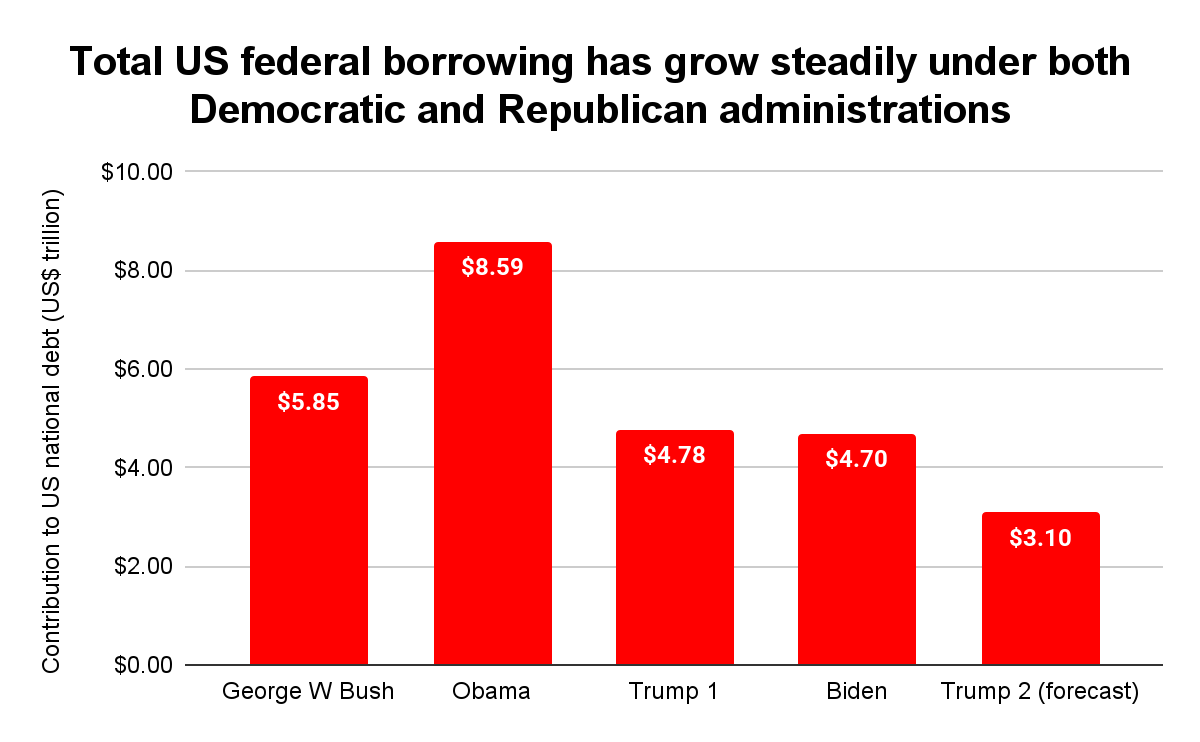

In an optically unfortunate coincidence, the bill was passed in the same week that Moody’s downgraded the US sovereign credit rating from AAA to Aa1. This makes it the third of the big three ratings agencies to do so, with S&P downgrading the US all the way back in 2013 and Fitch in 2023. This is not necessarily massive news, and nor is it entirely Trump’s fault. US federal borrowing has ballooned under both Republican and Democratic administrations, with Trump by some analyses actually adding less than his predecessors Biden and Obama.

But the rationale for the new tax plan is concerning. Trump’s team has justified this with a reheated version of the storied ‘trickle down economics’ argument, saying that lower tax rates would be offset by increases in investment and economic growth that would grow the tax base overall. The Council of Economic Advisors claims that the bill will increase real economic growth by 5.2% over the next four years, raising investment by 14.5% and adding up to 7.4 million jobs in the country.

History is not on Trump’s side here, and nor are many independent analyses. The Tax Foundation finds that the bill in its current form would increase GDP growth by only 0.6% and create only 794,000 new jobs (based on additional hours worked). But that is more than offset by the impact of lower receipts, mostly driven by lower rates and changes to tax banding.

There are many historical examples of the failed trickle down economics to choose from, but let’s take a simple one. In 1981, Ronald Reagan slashed the top rate of income tax from 70% to 50%, justifying this by saying that the cuts would pay for themselves as lower rates encourage more economic activity and more investment into the US. But this simply didn’t happen - Federal revenues fell by about 9% in the first couple of years, before Congress stepped in in 1982 and undid much of the tax cut.

The second part of this that is interesting is that they expose the tension between economic populism and small state tech-bro libertarianism within Trump’s MAGA coalition. While many of Trump’s wealthy donors and supporters in the business world cheer the tax and spending cuts, Trump’s base depends on working class Americans who depend on government programs like Medicaid and should be - in theory - against tax gifts to the country’s richest.

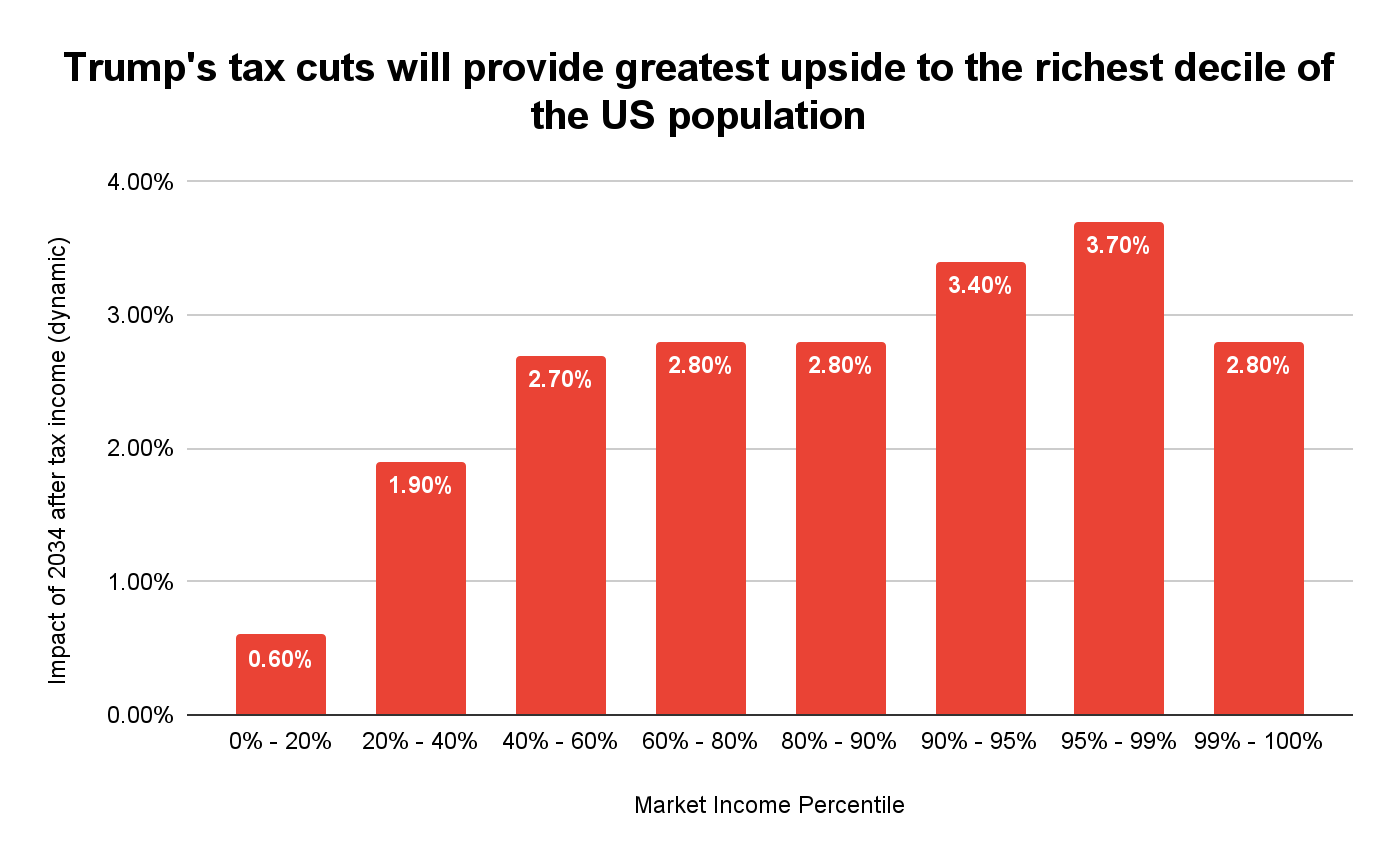

Even ignoring the cuts to welfare spending (we’ll get to those), the upside from income tax cuts would be felt much more strongly by the wealthy. The Tax Foundation forecasts that the post-tax income of the top 95 - 99% would be 3.7% higher in 2034 as a result of the cuts outlined by the House Ways and Means Committee, while those in the bottom 20% would see only 0.6% increases.

So the tax cuts themselves are going to increase inequality, even when we don’t factor in what they’ve taken away. But they’ve taken away a lot, mostly in the form of tightening eligibility requirements for Medicaid, the federal program to provide free healthcare to those on low income, and cuts to the Supplemental Nutrition Assistance Program (SNAP), which provides food stamps to low income families. The Congressional Budget Office (CBO) estimates that federal spending on Medicaid would fall by $698bn from 2026 - 2034, and SNAP by $267bn.

This will have a sharp impact on inequality. Cuts to Medicaid and SNAP would see the disposable income of the poorest decile of households fall by 2% by 2027, while for the richest decile it would increase by 4%, the CBO says.

The political ramifications of this for Trump will be very interesting to observe. As MAGA forefather Steve Bannon said on his podcast: “Medicaid, you’ve got to be careful with, because a lot of MAGA is on Medicaid. If you don’t think so, you are dead wrong. Medicaid is going to be a complicated one.”

Looks like tariffs are back on the menu

It’s come full circle. Only a couple of weeks after dismantling the last of his ‘Liberation Day’ tariff package after striking a trade deal with China in Geneva, Trump is banging the tariff drum again. On Friday, the president announced he planned to slap 50% tariffs on the EU, saying that the bloc was created “for the primary purpose of taking advantage of the United States on TRADE” and had been “very difficult to deal with” in recent talks. The methodology for the 50% number, which is well above the 20% the EU had initially been given under the original tariff package, is unclear.

Given his recent track record of trade-related U-turns, we cannot be confident that these tariffs will actually come into fruition (at the time of writing, he has just announced the tariffs will be delayed until July). However, it complicates the narrative that market turmoil has clipped Trump’s wings on this issue. It also shows that Trump either doesn’t understand or doesn’t care about the uncertainty it creates for US businesses. Perhaps the greatest risk now is that the US trade policy is entering a cycle of tariff, turmoil and retreat that has a very real economic impact on the very industries it is designed to protect.

Subscribe to our newsletter (for free)

Get the latest articles delivered right to your inbox.